What is the Difference Between Chapter 7 & Chapter 13 Bankruptcy?

We all encounter unexpected difficulties in life. Sometimes, those can take an extreme toll on our financial lives, making us feel like we’ll never recover from the situation. In those cases, the best thing we can do for ourselves is to declare bankruptcy.

But how does it work? What are the different types of bankruptcy, and which one better suits our current situation? How can we know if we’re even eligible to file for one?

In this article, we’ll discuss the answers to these questions in detail to help you choose the best path towards complete financial recovery.

Chapter 7 bankruptcy: the basics

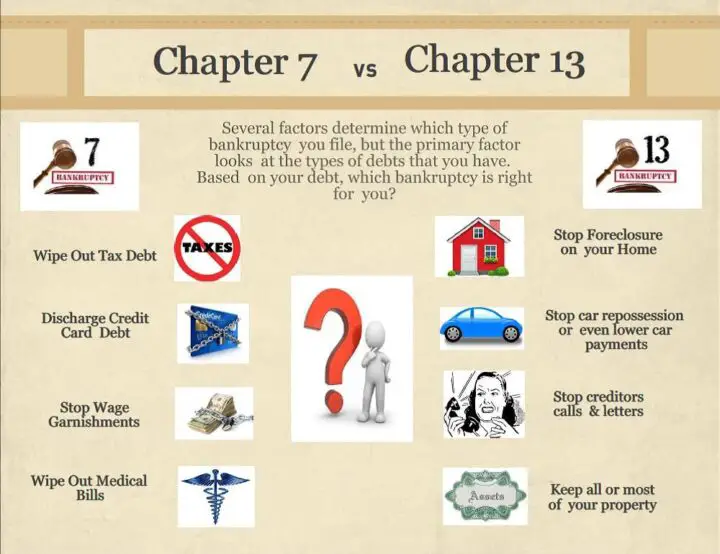

If you have little to no disposable income, you might want to consider filing for Chapter 7. It’s a type of liquidation bankruptcy in which you’ll have to sell most of your property to settle your debt and start anew. People who’re not homeowners and have limited incomes usually opt for Chapter 7 instead of Chapter 13 bankruptcy due to its speediness and since it doesn’t require you to follow a repayment plan. It’s available for both individuals and business entities alike, but it does have some drawbacks. You’ll have to be prepared to lose some assets along the way, and there’s no guarantee you’ll pass the eligibility test in the first place.

If you’re thinking about filing for Chapter 7 bankruptcy, we strongly recommend that you contact your lawyer beforehand to see whether it is an option for you or not. Many people waste their time only to fail the means test (their income is not low enough for them to be eligible).

Chapter 13: the basics

If you’d like to keep most of your assets while you’re undergoing bankruptcy, Chapter 13 might be a better option for you. Instead of selling your property to repay your creditors, you’ll be required to follow a strict monthly repayment plan until all of your debt is discharged. It will take you around 3-5 years to get your fresh start, but again, you won’t lose any of your property during the process. If you’re not sure you can handle the specified monthly payments for such a long time, you’ll be at risk of losing your Chapter 13 status, which could mean losing your assets too, so remember to be careful.

The monthly amount you’ll be required to pay mostly depends on your income, property and the type of debt you owe. We suggest you speak to a reliable attorney before you file for either type of bankruptcy since there are complex exemption rules in both cases that you need to know about first.

Overall, if your income is too large to qualify you for Chapter 7 or you’d rather not put your assets at risk, Chapter 13 might be the better alternative for you.

Chapter 7: The advantages

Again, a Chapter 7 bankruptcy is one of the most common types of bankruptcy available due to its remarkable ability to get you back on your feet in a matter of months. It’s especially beneficial to those who simply do not have enough disposable income to qualify for other types of bankruptcy instead.

Now, when we said you’d lose most of your assets by filing Chapter 7, we didn’t mean it literally. There are many types of property that can be protected by exemption laws (federal or state), so, no, you won’t lose everything you own during this process. In fact, if you have nothing to sell, your creditors won’t receive anything at all. We suggest you seek assistance from legal professionals such as those at AttorneyDebtFighters to check whether Chapter 7 bankruptcy makes sense in your case or not.

Lastly, if you’re in a hurry to get your life back on track, Chapter 7 bankruptcy can provide you with exactly what you need. Even though you’ll probably lose some of your assets during the process, once you finally break free from your debts, you’ll realize it was a rather small price to pay. Everything you’ve lost, you’ll be able to rebuild afterwards, so don’t worry about it right now. Focus on getting your financial situation in order first, and everything else will come into place later on.

Chapter 13: the advantages

The biggest advantage of Chapter 13 compared to its aforementioned counterpart has to be the absolute protection of your property during the process. All of your belongings will be safe and sound, while you’ll only have to sacrifice a portion of your income to get your debt erased. While yes, it might take a long time until you’re finally free of your debt, you’ll only have to pay the value of your non-exempt property, and your assets will be fully protected during the process.

If you’re a sole proprietor, you could file Chapter 13 for your business needs as well. Besides, if your income is simply not below the national/state average, you won’t be able to file Chapter 7 bankruptcy, which leaves Chapter 13 as your best alternative.

Now, we’ve said it before, and we’ll say it again: don’t make any moves until you’ve spoken with an attorney. They can help you make the best decision and reach the optimal outcome, all while keeping everything as quick and efficient as possible.

The conclusion

The main differences between Chapter 13 and Chapter 7 bankruptcies are as follows:

- Chapter 7 requires you to sell your property, while Chapter 13 requires you to follow a repayment plan issued by the court

- With Chapter 7, you’ll be debt-free in a matter of a few months, while Chapter 13 takes around 3-5 years to be finalized

- They have different effects on your credit score and different exemption rules

- Chapter 7 is for people with limited income, while anyone can file for Chapter 13

- Only sole proprietors and individuals can file for Chapter 13

Now, whichever you choose, make sure you’ve spoken to a lawyer beforehand. Different states have different requirements and rules, and only your local attorney can help you make the best choice for yourself.

We hope our article cleared up some things for you, and we wish you good luck in your journey of becoming debt-free!